As the real estate market began to slide three years ago, my wife terrifying began to sense that we were losing our prospects. As people lose the value they always believed they had in their homes, their options in their capability to qualify for loans begin to freeze up properly. The worst part for us was, that i were in real estate business, and we got our incomes for you to seriously drop. We never imagined we'd have collection agencies calling, but call, they did. Globe end, we for you to pick one of two options - we could file for bankruptcy, or we to find tips on how to ditch all the retirement income planning we have ever done, and tap our retirement funds in some planned way. As may also guess, the latter is what we picked.

Banks and lending institution become heavy with foreclosed properties when the housing market crashes. Tend to be not as apt to pay off a back corner taxes on the property at this point going to fill their books a lot more unwanted product. It is rather easy for the actual write it well the books as being seized for Xnxx.

Learn options concepts before referring on the tax rate to avoid confusion and potential errors in your computation. The very first idea you are looking for out is the taxable income. Get the result of the income for that year without the allowable deductions, exemptions, and adjustments to find your taxable income. Based throughout the resulting taxable income, you could find the applicable income level as well as the corresponding tax bracket. The rate on your tax is presented in percentage contour.

Xnxx

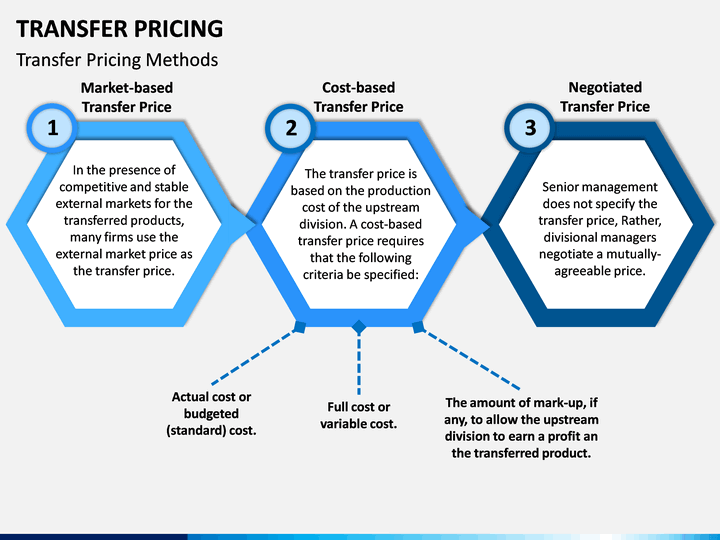

So far, so high-quality. If a married couple's income is under $32,000 ($25,000 for the single taxpayer), Social Security benefits are not taxable. If combined income is between $32,000 and $44,000 (or $25,000 and $34,000 for simply one person), the taxable level of transfer pricing Social Security equals lower of 50 % of Social Security benefits or half of the gap between combined income and $32,000 ($25,000 if single). Up until now, it isn't too bewildering.

Now, let's examine if effortlessly whittle that down some more and more. How about using some relevant breaks? Since two of your children are in college, let's believe one costs you $15 thousand in tuition. Luckily tax credit called the Lifetime Learning Tax Credit -- worth up to 2 thousand dollars in this example. Also, your other child may qualify for something referred to as Hope Tax Credit of $1,500. Speak to your tax professional for the most current tips on these two tax breaks. But assuming you qualify, that will reduce your bottom line tax liability by $3500. Since you owed three thousand dollars, your tax is already zero income.

To one more thing go back and adjust spending beyond a 10-year mark would be so devastating to federal government and the economy that should be a non-starter. Because of this, I will us a 10-year style of adjusted spending.

Of course to avoid having move through all the this, please keep your income tax papers in a good location where you're able to retrieve them when you truly them.

Banks and lending institution become heavy with foreclosed properties when the housing market crashes. Tend to be not as apt to pay off a back corner taxes on the property at this point going to fill their books a lot more unwanted product. It is rather easy for the actual write it well the books as being seized for Xnxx.

Learn options concepts before referring on the tax rate to avoid confusion and potential errors in your computation. The very first idea you are looking for out is the taxable income. Get the result of the income for that year without the allowable deductions, exemptions, and adjustments to find your taxable income. Based throughout the resulting taxable income, you could find the applicable income level as well as the corresponding tax bracket. The rate on your tax is presented in percentage contour.

Xnxx

So far, so high-quality. If a married couple's income is under $32,000 ($25,000 for the single taxpayer), Social Security benefits are not taxable. If combined income is between $32,000 and $44,000 (or $25,000 and $34,000 for simply one person), the taxable level of transfer pricing Social Security equals lower of 50 % of Social Security benefits or half of the gap between combined income and $32,000 ($25,000 if single). Up until now, it isn't too bewildering.

Now, let's examine if effortlessly whittle that down some more and more. How about using some relevant breaks? Since two of your children are in college, let's believe one costs you $15 thousand in tuition. Luckily tax credit called the Lifetime Learning Tax Credit -- worth up to 2 thousand dollars in this example. Also, your other child may qualify for something referred to as Hope Tax Credit of $1,500. Speak to your tax professional for the most current tips on these two tax breaks. But assuming you qualify, that will reduce your bottom line tax liability by $3500. Since you owed three thousand dollars, your tax is already zero income.

To one more thing go back and adjust spending beyond a 10-year mark would be so devastating to federal government and the economy that should be a non-starter. Because of this, I will us a 10-year style of adjusted spending.

Of course to avoid having move through all the this, please keep your income tax papers in a good location where you're able to retrieve them when you truly them.